You hear it almost daily now.

The economy is strong.

Inflation is cooling.

Growth is steady.

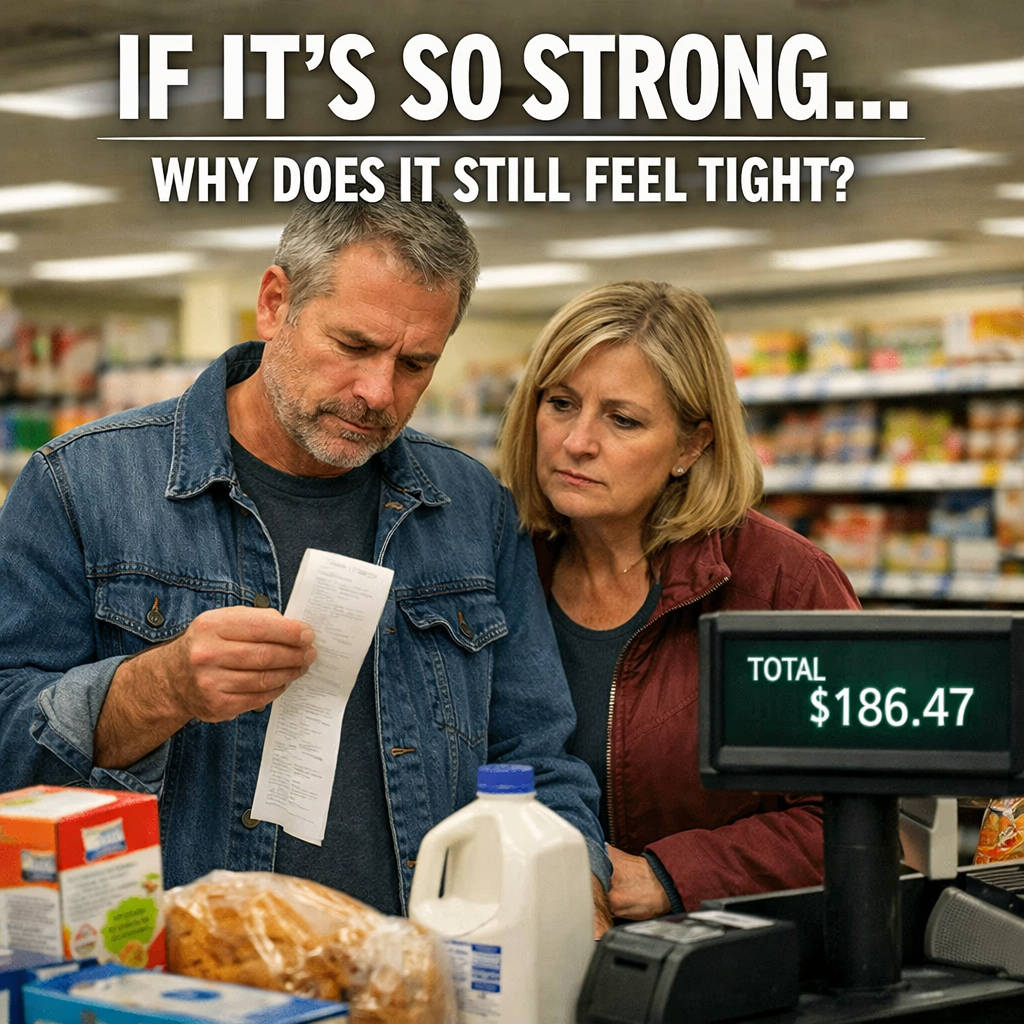

And yet, at the grocery store, the total still makes you pause.

A cart that used to cost $120 creeps toward $170.

Insurance renewals come in higher — again.

Property taxes inch upward.

A basic repair feels like a financial event.

You don’t need a spreadsheet to know something feels off. You feel it when you swipe your card.

That’s why a recent national poll showing that more than 80% of Americans say affordability hasn’t improved doesn’t surprise most people. Nearly half say it’s actually worse. And these aren’t fringe opinions. They’re middle-income families. Working parents. Retirees on fixed budgets. People who don’t live in headlines — they live in monthly bills.

This isn’t about party loyalty. It’s about pressure.

Part of the confusion comes from how we talk about inflation. When officials say inflation is “down,” they mean prices are rising more slowly than they were before. That’s good. But it doesn’t mean prices went back to where they started. It just means they’re climbing at a gentler slope.

If a gallon of milk jumped from $3 to $5, and now it rises to $5.25 instead of $6 — inflation slowed. But your grocery bill didn’t shrink. It just stopped accelerating as fast.

Technically better. Practically still expensive.

Wages have risen in some sectors. Unemployment remains relatively low. Markets have had strong stretches. Those things matter. But most households don’t experience the economy through stock indexes or quarterly GDP. They experience it through rent, gas, insurance premiums, school fees, and the quiet math they do in their heads before every purchase.

That’s where the disconnect lives.

When leaders describe a “strong economy,” they’re often talking about macro indicators. But when families evaluate the economy, they’re asking a different question:

Do I feel more stable than I did two years ago?

Stability is harder to measure. It doesn’t show up cleanly in a press release. It’s the feeling that you can handle a car repair without rearranging the month. That your kid might someday afford a house without your help. That retirement won’t require constant recalculation.

For many Americans, that sense of stability still feels thin.

There’s also a generational layer to this conversation. Younger families are delaying homeownership. Parents are quietly helping adult children with rent. Retirees are watching savings more carefully than they expected to at this stage of life.

A strong nation isn’t measured only by growth charts. It’s measured by whether the next generation believes they’re stepping onto solid ground.

That belief feels shaky for a lot of people.

None of this means the economy is collapsing. It isn’t. But strength that only shows up in data tables, and not in daily life, starts to feel abstract. When messaging and lived experience drift apart, trust erodes — not overnight, but slowly. Like a floorboard that softens one season at a time until you finally notice it bending.

People don’t expect perfection. They understand economies move in cycles. What unsettles them is being told things are better when their own math suggests otherwise.

Maybe the real question isn’t whether the economy is technically improving.

Maybe it’s whether improvement is reaching the people who were promised it would.

Because if most Americans still feel like they’re treading water, then calling it a golden age won’t make it feel that way.

And until everyday life feels lighter — not just statistically stronger — that gap between message and reality will remain.

And people will keep asking, quietly and reasonably:

If it’s so strong… why does it still feel tight?