Drive through enough small towns and the story is visible without a single statistic. A factory that once ran three shifts now sits silent. A hardware store boarded up. A hospital wing closed. Families stretching paychecks thinner each month while groceries, insurance, and rent keep climbing.

Then open a financial report and see another headline: a new billionaire minted.

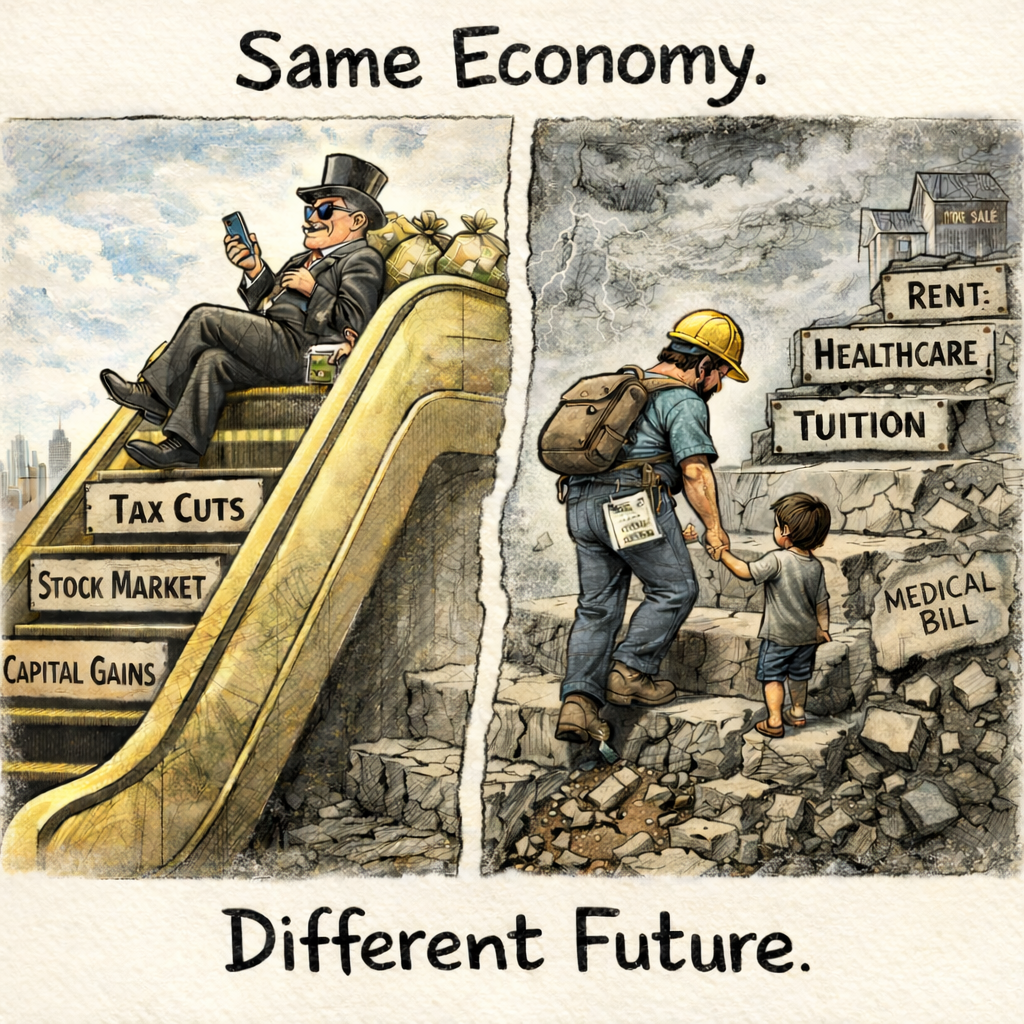

That contrast is not accidental. It is the product of choices — decades of economic decisions rooted in the belief that prosperity flows downward from the top.

In the early 1980s, America had fewer than 20 billionaires. Today there are more than 700 in the United States alone, according to Forbes. Globally, the number exceeds 2,500. The rise has been extraordinary.

At the same time, wealth has concentrated at levels not seen in generations. Federal Reserve data show the top 1% now control roughly 30% of total household wealth. The bottom half of the country holds about 2–3%.

This did not happen overnight. It happened by design.

The modern supply-side experiment accelerated during the presidency of Ronald Reagan. The top marginal income tax rate, which stood at 70% in 1980, was cut to 28% by the end of that decade. Corporate taxes declined over time. Capital gains taxes — the tax on profits from investments — were often kept lower than taxes on wages.

The theory was simple: free up capital, reward investment, and growth will follow. Growth would lift everyone.

Growth did come. GDP expanded. Markets soared. Since 1980, the S&P 500 has risen more than twentyfold.

But the rewards did not spread evenly.

The Federal Reserve reports that the top 10% of Americans own nearly 90% of all stocks. When markets surge, wealth surges — but it surges upward.

Meanwhile, the Economic Policy Institute finds CEO compensation has grown more than 1,000% since 1978, adjusted for inflation. Typical worker pay has grown roughly 15–20% in that same period. Productivity climbed. Profits climbed. Executive pay exploded. Worker wages barely moved.

No one is arguing that success should be punished. But this is not balance.

Since 1980, college tuition has risen several times faster than inflation. Healthcare spending per person has more than tripled in real terms. Home prices, especially in the past few years, have far outpaced wage growth. The cost of stability has risen faster than the ability to earn it.

When manufacturing plants closed across the Midwest and South, communities were told new industries would replace them. Some regions prospered — particularly technology and finance hubs. But many towns were left with fewer jobs, shrinking tax bases, and young people moving away.

At the same time, industries consolidated. Airlines merged. Banks merged. Meatpacking consolidated. Technology platforms absorbed competitors. In sector after sector, market power narrowed to a handful of dominant players.

Wealth concentrated. Power concentrated. Influence followed.

Campaign finance data show political giving is heavily skewed toward high-income donors. That does not automatically mean corruption. But it deepens a public sense that access and influence increasingly track net worth.

The central issue is not whether billionaires should exist. It is whether an economic system that produces extraordinary gains at the top while leaving half the country with minimal savings is sustainable.

An economy is not just GDP. It is whether a truck driver can afford a home near work. Whether a nurse can pay off student loans before middle age. Whether a machinist believes their children will live better than they did.

For forty years, Americans were told prosperity would trickle down.

What is clear now is that much of it pooled at the top.

And a country cannot remain steady when the distance between its peaks and its foundation grows this wide.